Walter Shannon

https://shannon-law.com/wp-content/uploads/FullSizeRender.jpg

514

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-11-27 10:50:512019-11-27 11:04:59Talking Point: Donating your IRA or other Qualified Plan to Charity Upon Death

Walter Shannon

https://shannon-law.com/wp-content/uploads/FullSizeRender.jpg

514

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-11-27 10:50:512019-11-27 11:04:59Talking Point: Donating your IRA or other Qualified Plan to Charity Upon Death https://shannon-law.com/wp-content/uploads/22448236_1486552321380725_1306012863419026157_n-1.jpg

583

960

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-05-30 14:01:222019-08-20 19:09:06How do I Open and Manage a Probate?

https://shannon-law.com/wp-content/uploads/22448236_1486552321380725_1306012863419026157_n-1.jpg

583

960

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-05-30 14:01:222019-08-20 19:09:06How do I Open and Manage a Probate? https://shannon-law.com/wp-content/uploads/lake-placid-inn2.jpg

808

1215

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-05-23 15:13:162019-11-27 11:23:12Who gets the personal property when the Family Cabin is sold?

https://shannon-law.com/wp-content/uploads/lake-placid-inn2.jpg

808

1215

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-05-23 15:13:162019-11-27 11:23:12Who gets the personal property when the Family Cabin is sold? https://shannon-law.com/wp-content/uploads/bankers-cabinet.jpg

1512

2016

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-03-02 03:10:262019-08-20 19:09:47Should I tell my insurance agent that my house is going into my trust?

https://shannon-law.com/wp-content/uploads/bankers-cabinet.jpg

1512

2016

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-03-02 03:10:262019-08-20 19:09:47Should I tell my insurance agent that my house is going into my trust? https://shannon-law.com/wp-content/uploads/workers-1.jpg

276

460

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-02-17 00:29:242019-08-20 19:10:22What is a Wisconsin Transfer on Death Deed?

https://shannon-law.com/wp-content/uploads/workers-1.jpg

276

460

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-02-17 00:29:242019-08-20 19:10:22What is a Wisconsin Transfer on Death Deed? https://shannon-law.com/wp-content/uploads/broken-heart.jpg

2016

1512

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-02-16 21:38:332019-08-29 09:50:00Contentious Probate Settled – Kudos to the Family Involved

https://shannon-law.com/wp-content/uploads/broken-heart.jpg

2016

1512

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2019-02-16 21:38:332019-08-29 09:50:00Contentious Probate Settled – Kudos to the Family Involved https://shannon-law.com/wp-content/uploads/IMG_9845.jpg

480

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

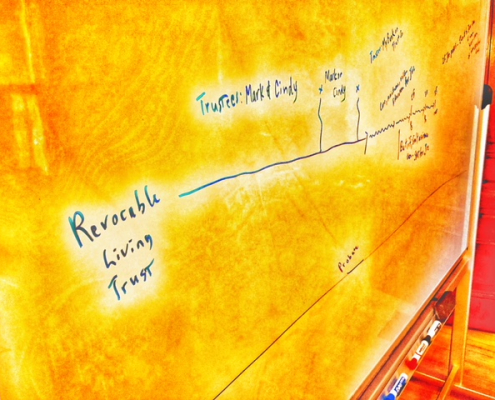

Walter Shannon2018-08-29 13:26:552019-08-20 19:11:13Revocable living trust and pour over will. Why do I need both?

https://shannon-law.com/wp-content/uploads/IMG_9845.jpg

480

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-08-29 13:26:552019-08-20 19:11:13Revocable living trust and pour over will. Why do I need both? https://shannon-law.com/wp-content/uploads/grunge-books.jpg

640

480

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-06-09 01:03:282019-08-20 19:11:31News Flash: Beneficiary designations are a Big DealWalter Shannon

https://shannon-law.com/wp-content/uploads/FullSizeRender.jpg

514

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-02-20 18:40:282019-11-27 11:41:55Estate and Trust Planning: Going Beyond Just the Numbers and into the Heart

https://shannon-law.com/wp-content/uploads/grunge-books.jpg

640

480

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-06-09 01:03:282019-08-20 19:11:31News Flash: Beneficiary designations are a Big DealWalter Shannon

https://shannon-law.com/wp-content/uploads/FullSizeRender.jpg

514

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-02-20 18:40:282019-11-27 11:41:55Estate and Trust Planning: Going Beyond Just the Numbers and into the Heart https://shannon-law.com/wp-content/uploads/desk.jpg

960

752

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-12-19 20:45:132019-08-20 19:13:03Choosing an Attorney for Your Estate Planning

https://shannon-law.com/wp-content/uploads/desk.jpg

960

752

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-12-19 20:45:132019-08-20 19:13:03Choosing an Attorney for Your Estate Planning https://shannon-law.com/wp-content/uploads/22310612_1490054057697218_7619024954823394515_n.jpg

580

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-10-24 01:06:392019-11-27 11:49:30Conservation Easement: A Beautiful Thing

https://shannon-law.com/wp-content/uploads/22310612_1490054057697218_7619024954823394515_n.jpg

580

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-10-24 01:06:392019-11-27 11:49:30Conservation Easement: A Beautiful Thing https://shannon-law.com/wp-content/uploads/22448236_1486552321380725_1306012863419026157_n-e1701379969363.jpg

382

960

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-10-24 00:51:112019-08-20 19:14:40News Flash: Few People Actually Plan for Death or Incapacity

https://shannon-law.com/wp-content/uploads/22448236_1486552321380725_1306012863419026157_n-e1701379969363.jpg

382

960

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-10-24 00:51:112019-08-20 19:14:40News Flash: Few People Actually Plan for Death or Incapacity https://shannon-law.com/wp-content/uploads/Irrevocable-Trusts.png

390

358

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-08-15 17:39:292019-08-20 19:15:01Why did you put Latin in my Will and Trust?

https://shannon-law.com/wp-content/uploads/Irrevocable-Trusts.png

390

358

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2016-12-06 20:07:302016-12-06 20:07:30Compressed Tax Brackets on Irrevocable Trusts

https://shannon-law.com/wp-content/uploads/grunge-books.jpg

640

480

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2016-04-12 20:48:012019-11-27 11:36:59Got Will?

https://shannon-law.com/wp-content/uploads/Irrevocable-Trusts.png

390

358

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2017-08-15 17:39:292019-08-20 19:15:01Why did you put Latin in my Will and Trust?

https://shannon-law.com/wp-content/uploads/Irrevocable-Trusts.png

390

358

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2016-12-06 20:07:302016-12-06 20:07:30Compressed Tax Brackets on Irrevocable Trusts

https://shannon-law.com/wp-content/uploads/grunge-books.jpg

640

480

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2016-04-12 20:48:012019-11-27 11:36:59Got Will?