Tag Archive for: revocable living trusts

https://shannon-law.com/wp-content/uploads/IMG_9845.jpg

480

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-08-29 13:26:552019-08-20 19:11:13Revocable living trust and pour over will. Why do I need both?

https://shannon-law.com/wp-content/uploads/IMG_9845.jpg

480

640

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-08-29 13:26:552019-08-20 19:11:13Revocable living trust and pour over will. Why do I need both? https://shannon-law.com/wp-content/uploads/grunge-books.jpg

640

480

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-06-09 01:03:282019-08-20 19:11:31News Flash: Beneficiary designations are a Big Deal

https://shannon-law.com/wp-content/uploads/grunge-books.jpg

640

480

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2018-06-09 01:03:282019-08-20 19:11:31News Flash: Beneficiary designations are a Big Deal https://shannon-law.com/wp-content/uploads/Revocable-Living-Trust.jpg

1070

1200

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

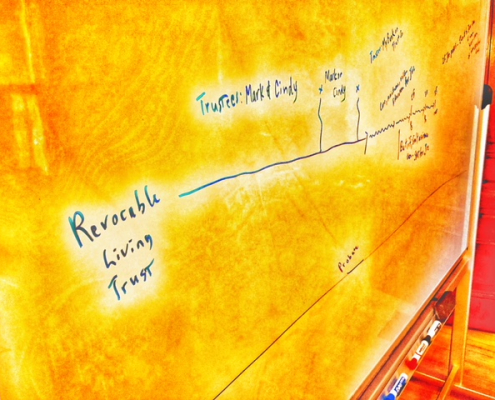

Walter Shannon2016-06-22 15:37:192016-07-08 13:57:54Trusts: How Do I Ascertain the Ascertainable?

https://shannon-law.com/wp-content/uploads/Revocable-Living-Trust.jpg

1070

1200

Walter Shannon

https://s3.amazonaws.com/shannon-law.com/wp-content/uploads/20190821102841/logo-rebuild.gif

Walter Shannon2016-06-22 15:37:192016-07-08 13:57:54Trusts: How Do I Ascertain the Ascertainable?